Comparing Healthcare Service Utilization in Insured vs Non Insured Households in Rural Atsbi Womberta

Community-based health insurance schemes (CBHI) in Africa are gaining attention due to high healthcare costs in developing nations, affecting 6% of individuals in extreme poverty. The World Health Organization emphasizes the need for sustainable health funding schemes to ensure access to health services. Ethiopia faces poor healthcare funding, making it one of the world’s poorest nations. Tigray implemented community-based insurance as a pilot study in 69 rural communities since 2010. The objective of this study was compare differences in healthcare service utilization between community-based health insurance among insured and non-insured households in rural Atsbi-Wemberta district. A community-based comparative cross-sectional study with a qualitative approach was conducted on 172 households. Data was analyzed using SPSS, and inferential statistics were used to measure factors’ association with outcome variables. A study in Kebelle revealed that the majority of respondents were female-headed, engaged in both insurance schemes, and had higher education levels. Marital status was also significant, with 89% living with their families. The majority were married, with 91.8% insured and 86.0% uninsured. Family size and income were significant factors, with high-salary households less likely to be members of the Community Based Health Insurance (CBHI) scheme. The study found that most participants considered themselves intermediate healthcare providers, with limited service due to affordability and segregation. The study suggests increasing healthcare service utilization by introducing Community Benefits Health Insurance (CBHI) to improve access to healthcare and promote good governance. However, the study faces criticism for unfairness and insufficient benefits for non-insured participants. Household were enrolled in CBHI (56.2%) were more probable to use health care service than households who were not enrolled (43.8%) (χ2=21.359, p<0.001). Community Benefits Insurance (CBHI) has increased healthcare utilization among insured households due to reduced illness costs and increased healthcare professional involvement. Factors like income, family size, and travel time contribute to higher utilization. However, challenges include lack of knowledge and community awareness.

Introduction

“Health” means complete physical, social, and psychological well-being, not just the absence of disease. It includes social and mental dimensions and extends beyond just physical capacity or dysfunction [1]. Healthcare refers to a nation’s provision of various mechanisms to treat physically and mentally ill individuals [2]. Insurance is a contract that protects from harm and loss. Health coverage is a type of insurance that covers medical expenses [3]. It provides protection against medical expenses through various insurance programs to enhance public healthcare.

The Community-based health insurance scheme (CBHI) is a voluntary, non-profit system that provides cash access during illness to the impoverished and informal sector, funded by member contributions or premiums [4]. The potential benefit of the systems lies not only in mobilizing resources but also in improving and organizing health services [5]. Advocates argue that Community-Based Health Insurance (CBHI) schemes can provide financial protection for low-income populations against healthcare expenses. This is especially valuable for reaching a significant number of homeless individuals who would otherwise lack economic security to cover the costs of illness [6]. However, critics claim that the risk pool is often too low, that adverse selection problems occur, that systems are highly reliant on subsidies that economic and operational problems occur and that sustainability in general not guaranteed [7].

Globally, 400 million people lack access to quality health services due to financial barriers and poverty [8]. Only one in five citizens, however, takes steps to protect against financial expenditure, including obtaining health insurance coverage [9]. People experiencing financial difficulties may forgo using healthcare facilities; for example, the link between access to healthcare, financial payments, and marginalization. It highlights the variations in healthcare systems between high-development and low-economic countries and the importance of resource mobilization and financial security for healthcare [10].

In Africa, CBHI systems have gained renewed interest. Communities are being engaged to expand risk-pooling coverage for informal sectors and rural populations [11]. As a result, 6% of developing nation individuals falls into extreme poverty due to healthcare costs [12]. Social problems in health outcomes and service usage rates persist in many nations, indicating that universal health coverage (UHC) equity principles are not being met in both community groups [13].

In 2005, the WHO issued a joint statement on sustainable health funding and the need for health funding schemes in many nations to ensure access to health services [14]. In addition, Pre-payment and pooling of resources and risks are essential for managing financial risks, and the quality of a health financing system should be tailored to each country’s specific context [15]. This resolution tackles Africa’s major issue of out-of-pocket healthcare payments. Nearly 60% of African healthcare is paid by individuals, leading to poverty cycles [16].

However, CHI is struggling with low enrollment rates in sub- Saharan Africa, due to limited access to quality healthcare services, inefficient payment systems, and limited options. Only 5-10% of the population has access to health insurance coverage, compared to up to 26% in middle-income countries [17].

Ethiopia’s health expenditure is insufficient compared to other nations, making it one of the world’s poorest in terms of healthcare funding [18]. In 2011, the Ethiopian government introduced two health insurance schemes. The first, social health insurance is mandatory for the formal sector and retirees, funded by contributions from salaries and pensions [19]. In the design stage, social health insurance has not yet been implemented. The CBHI system aims to improve access to care and reduce out-of-pocket healthcare costs for rural communities and informal settings, targeting 83.6% of the population [20].

Since June 2011, the Ethiopian government has been implementing the Community-Based Health Insurance (CBHI) in thirteen areas. Three years later, the program expanded to over 100 districts, benefiting approximately 300,000 households. However, not all families were officially enrolled in CBHI [21].

The pilot program had a 52% national enrollment rate and received contributions from approximately 85 demographic segments. The remaining member was financially supported by various public sectors. Access to essential healthcare services has improved, leading to better overall healthcare [22]. In 2011, studies on the post-CBHI scheme showed a negligible increase in health service use for insured families and a decrease for non-insured families. Evaluating factors influencing healthcare service use can help in implementing improvements [23]. In Ethiopia, CBHI is supported. Insured individuals receive better healthcare than uninsured ones. Insured family heads are better off than those who are not eligible for household services [24]. The Community-based health insurance scheme therefore had the potential to deliver universal coverage of health services through risk pooling and to protect rural families and the informal sector from costly spending on health care [25].

Hence, Tigray is one amongst the chosen regions that have implemented community-based insurance as a pilot study in different districts based on their criteria and feasibility. For example, distance from health institutions, socioeconomic status, and perceived quality health care factors. Within the same study, Tigray regional health bureau survey carried out a survey since the year of 2010, about 69 rural communities’s kebelle of the district have begun and established a pilot test among a voluntary membership of prelude activity. While the introduction of CBHI, Hence, the importance between the enrollment and health care service utilization among family heads have not well measured by most members of the community. Therefore, this study was identified the difference in enrollment and to show the link between CBHI enrollment and health care service utilization in rural Atsbi-Womberta district.

Statement of the Problem

Good health is important. People seek modern healthcare services to avoid illness and injury. Healthcare establishments provide treatment for ailments and services for better health [26]. Healthcare cannot be bartered. Although it is possible to provide some economic support to offset the loss of health status, ill health cannot be fully compensated. There are limits to this, and people cannot be insured or subsidized for their death [27].

Insurance covers healthcare costs for individuals with poor health. The coverage is not based on the usefulness of healthcare services, except when ineffectiveness is due to neglect. Ambiguous treatments are usually not covered [28].

Health care for informal sector workers is a major challenge in many developing countries [29]. Despite notable attempts by many developed countries to address these problems, they stay behind as serious obstacles to overall economic growth [30]. Illness without proper health insurance can lead to financial strain on families, increasing the risk of abandoning treatment or resorting to low-quality healthcare [31]. Globally, over 150 million individuals face financial hardship due to health costs every year, with 100 million people falling below the poverty line after paying for their healthcare expenses [22] and 1.3 billion people living with low incomes lack access to effective healthcare. This pushes them into poverty, especially in developing countries where payments are made out-of-pocket [32] Poverty can cause health issues due to lack of access to medical care and proper living conditions.

In Africa, health costs are mostly paid out-of-pocket by individuals, ranging from 30 to 85% of the total healthcare expenses. This can be very costly and often leads to poverty. Healthcare costs are the primary reason why households struggle financially [4].

In sub-Saharan African countries, Ethiopia has the lowest percentage of health service consumption with only 6% utilization of inpatient healthcare [33], only 1.2% of people had both personal and public health insurance, according to the findings [34]. The existing health insurance only covers the formal sectors which account for only 10% of the populace. The UNDP 2010 report indicates that personal life expectancy is about 56 years, infant mortality rate is 71.2/1000 live births, less than five-year death is 112/1000 and maternal deaths are 470/100,000 live births [35]. According to the EDHS report, in 2011, only a slight improvement was observed in the per capita use of outpatient healthcare services compared to 2000. Additionally, there were significant gaps in antenatal care for pregnant women, skilled health workers attendance during births, and access to treatment for children under five with respiratory illness and fever [36]. High out-of-pocket spending (37%) on healthcare leads to low utilization rates and inadequate healthcare provision [37].

In the Tigray region, the overall enrolment rate is very low but the highest percentage of needy households are found, so that, the status of health care services utilized remains very pathetic [38], Victims are made up of around 72.5% of people who look for advanced healthcare services [39]. Poverty is widespread in Atsbi-Wemberta, particularly among rural households. Scarcity of job opportunities and low productivity due to insufficient rainfall exacerbate the community’s health issues, exposing people to various diseases and health risks [3]. Limited healthcare services and economic constraints reduce access to healthcare.

To Since 2011, the government has implemented CBHI to promote the health of poor rural residents by sharing the financial burden of healthcare provision [21]. As therefore, CBHI is regarded as a possible tool for reducing the consequences of poverty linked to health care costs. Nevertheless, there hasn’t been much research done on how CBHI affects the use of healthcare services. As a result, the goal of this study was to determine the factors influencing CBHI enrolment in the rural Atsbi-Wemberta district and to assess healthcare utilization discrepancies between households with and without insurance.

Objective of the Study

General Objective

The objective of this study was comparing healthcare service utilization in insured vs. non-insured households in Rural Atsbi womberta

Specific Objectives

- To determine the community perception towards the implementation of CBH in rural Atsbi-Womberta district

- To identify factors associated with healthcare service utilization among insured and non-insured households of rural Atsbi-Womberta district.

- To determine the healthcare seeking behavior towards healthcare service utilization.

Significance of the Study

Community-based health insurance (CBHI) is a beneficial scheme that helps individuals tackle financial health problems and maximizes their health. Atsbi-Womberta district is one of the districts that have implemented CBHI as a pilot study. This study aims to compare the differences in healthcare service utilization and CBHI between insured and non-insured households. The purpose of this research is to explore how CBHI schemes can contribute to national policy and how different CBHI designs and government policies can affect policy objectives. It will also help governments provide an alternative to healthcare to ensure equal healthcare services for the community and make insured households feel safe by comparing payment and services while narrowing the gap observed during the implementation time. Furthermore, it will contribute to understanding different cultures and environments and serve as a pathway to attain Universal Health Coverage (UHC) by promoting equitable access through best practices in the community. This study will also provide significant input to previously conducted research on the same ground. Therefore, the scheme is helpful to governments in creating large risk pools to cover the health costs of individuals who cannot afford to contribute.

Operational Definitions

Health: “Wellness is not just the lack of disease, its complete physical, mental, and social well-being [1]”. Community- based health insurances scheme: This framework provides financial insurance against illness or disability and improves access to healthcare for low-income rural households without formal insurance [4]. Household: People living together, sharing meals. Insured Household: Households included in the CBHI system are protected by a health insurance policy. Non-insured Household: Are households who are not members of the CBHI scheme. Utilization of health care: Healthcare utilization is measured by at least one household member visiting health services in the past 6 months [40, 41].

Scope of the Study

The CBHI scheme deals with healthcare issues that are relevant to the rural community. This survey was conducted in the Atsbi-Wemberta district at five kebelle. However, the study faced certain limitations due to time constraints and the availability of participants, which affected its success. The study aimed to examine how the healthcare service utilization was impacted by the implementation of the scheme. It also looked at the factors that influenced the enrollment status of individuals in the scheme. A mixed type of research was conducted on 172 households, which were individually selected for the study.

Materials and Methods

Research Design

A community based comparative cross-sectional study design mixed with qualitative type of approach was used in this study.

Description of Study Area

Atsbi-Wemberta is a district located about 860 km north of Addis Ababa and 65 km northeast of the capital city of Tigray, which is Mekelle. The district comprises of 18 kebelle administrations and has a total population of 133,811, consisting of 63,599 males and 70,212 females. The district has 30,605 homes, out of which 4,390 households are enrolled in the CBHI scheme. Every member of the CBHI has registered in the Muster Book. The participants who are insured under the CBHI scheme do not have to pay directly for their healthcare services. The district has 15 health posts, 4 health centers, and one hospital. According to statistics, one health post is expected to serve 5,000 people, while one health center can provide services to 25,000 people. The majorities of the people in the district live in pastoral areas and rely on farming. The implementation of CBHI began in the district in 2011 (Sources: from Atsbi-Wemberta Woreda health office, 2014) (Figure 1).

Population and Sample Size

Source of Population

All insured and non-insured household who live in Atsbi- Wemberta district.

Study Population

Sampled of insured and non-insured households who are greater than 18 years old from the randomly selected five kebelle were included.

Sampling and Sampling Procedure

Sample Size Determination

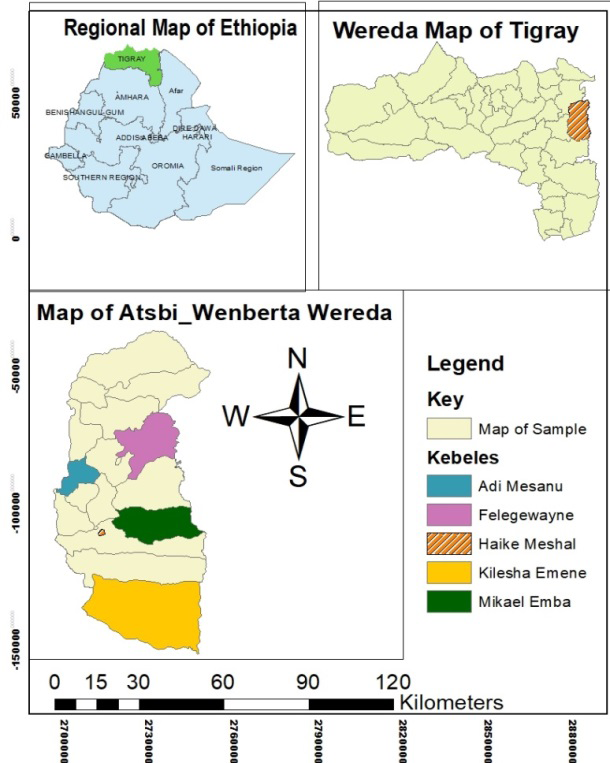

This study was applied an easy formula provided [41] to work out the required sample size. An available similar study was used at 95% CI, and level of precision=0.5% (0.05 of marginal error); n=N/ (1+N (e) 2) Where; n is Indicated the sample size, E is Shows the appropriate sampling error and N is labeled the total population at 95% confidence interval, p=0.05 can take into an account at significant level. The calculated sample size was included from each insured and non-insured household families by considering 10% non-response rate. Hence, the ultimate sample size was 156 households (78 from insured households and 78 non-insured household participants were taken purposely in order to compare and manage the raw data) and 16 households were thought-about as non- respondent rates because of an absence or refusal to reply. Therefore, the calculated sample size was 172 households from 8549 selected households. This implies that 1735 insured and 6814 were the non-insured family heads from the total household size (30,605) calculated through PPS (Probability Proportion to Sample Size) that has found within the district [41, 42]. To calculate the ordinal value of the sample size (the number of insured households and non-insured households inside the population divided by the number of households needed for the sample). To begin the data collection, it is useful to use this formula since a systematic sampling method was used. Therefore, the kth = N/n; the kth of insured and non-insured households= total number of insured households /sample size of insured households=1735/78=22th. Once the list was formed, each 22th home on the list was chosen as a participant. Sampled households proportionally allocated to each sampled kebelle. Moreover, in every kebelle households were proportionally allocate based on the insurance recognition (insured and uninsured) and was systematically be decided on. Then to start the data collection any number was picked using lottery method from the list of households [43].

| No | Selected kebelle | Area in hectare | No of insured house hold | No of non- insured house hold | Total household | Sample insured households | Sample non- insured households | Total Sample household |

|---|---|---|---|---|---|---|---|---|

| 1 | Mikael emba | 7639.19 | 350 | 1440 | 1790 | 16 | 16 | 32 |

| 2 | Haike meshal | 101.71 | 513 | 735 | 1248 | 23 | 8 | 31 |

| 3 | Felegwa yne | 7568.13 | 384 | 1672 | 2056 | 17 | 19 | 36 |

| 4 | Kilesha emene | 20929.43 | 433 | 1138 | 1571 | 19 | 13 | 32 |

| 5 | Adi Mesanu | 2662.4 | 55 | 1829 | 1884 | 3 | 22 | 25 |

| Total | 1735 | 6814 | 8549 | 78 | 78 | 156 |

Table 1: Sampling table.

Owned Designed

Here in the table 1, the calculated sampled size from the insured HH was 78 from (N=1735). Likewise, the sample size of non-insured household was the same as the insured household, which means that, which was taken purposely in order to compare with insured HH. What is more, apart to the above survey, three FGD were structured. Every FGD has eight members, where the two FGDs have considered as insured member and the third one has composed of four insured and four non-insured HH member. Besides, five key informant interview (KII) were introduced with kebelle head managers as well as with Woreda CBHI coordinators taking into consideration of their experience the way in which they provides the service and contacting with the kebelle workers as well as with every HH of the community. As completely different scholar place their argument relating to concerning the formulation of the FGD members with their specific numbers, for example a scholar referred by Onwuegbuzie (2009) as elucidate that, the rang need to stuck between six to eight is an eligible criteria. In addition, an alternate plan is offer by O.Nyumba et al enlighten that, to possess a top quality focus group discussion it ought to be between eight to ten participants per session. By having the construct of the on top of listed scholars, the investigator compelled to come to a decision to use a mean of eight participants per session.

In this survey, members who are participated once within the FGD (1) were not collaborating in ordinal and third FGD. Here the KII and FGD elite through purposefully because of by considering they are the potential supply of knowledge (Table 1).

Sampling Technique and Procedure

A mixed-type of comparative cross-sectional study was commanded to work the data collection, to analysis and to interpret the relevant data properly. The study populations were randomly selected from the list of total kebelle found in Atsbi-Wemberta district. Form the total households, five kebelle were taken to realize the entire sample of the households. In the first stage, five kebelle (8549 households) were selected via simple random sampling out of 18 rural kebelle found in the district. These are; Mikael-Emba, Haike-Meshal, Felege-Wayne, Kilesha and Adi-Mesanu. Of the selected kebelle, 1735 were insured and 6814 are not included in the scheme. The Data were obtained from Atsbi- Wemberta district of CBHI coordinating work office. To select the insured and non-insured households were based on their family folder range. In the next stage, households were allocated proportionally by practicing systematic random sampling. The primary households were chosen randomly from the list of households’ family folder numbers. A multi- stage type of sampling technique was practiced to hold out all the entire units found within the population. Because the investigator wants to focus such as variables like; age, sex, education, etc. simple random sampling was used to select kebelle from completely different subgroups using the proportional sampling method [6]. So that, to induce the inured-uninsured households, simply, the researcher inspired to pick out the list of households through using systematic random sampling to selected both insured and non-insured households. The user and non-user households were obtained from the CBHI head office managers. Finally, households were randomly selected to start the data collection from any number from the list frame of CBHI members and non-member family heads.

Selection Criteria

Inclusion Criteria

Both insured and non-insured households with those who are greater or equal to 18 years old were included in the study.

Exclusion Criteria

Household heads who do not appear to be able to communicate or households’ with critically sick family heads were excluded from the study. Additionally, those who have not permanent identity card and participant who are working in the2formal organization were not engaged in the study.

Tools (Instruments)

Quantitative Elements which have an effect at once to health care service and disparity in the provision of quality of health care service in the direction of the contribution health care service among household found in rural part of Ethiopia. Conquering socioeconomic with specific related barriers, specially, are importantly to get the proper of access to the health care is not only result of remedial or clinical checkup but decide what we are doing as human to generate the surroundings in which humans may be hold in an accurate physical form. Therefore, to carry out the data collection instrument like self-prepared assessment questionnaire, KII and FGD were used as the main gadget to manipulate the whole method.

Measurement of HSB and Heath Care Service Utilization with Multiple Causal Factor This sophisticated measure helped to analyze by introducing the CBHI in order to enhance the health care service utilization among the agricultural households by measuring the health- seeking behavior among households through supporting and motivating both insured and non-insured households to become a member of the scheme. These composite measures of perceived HSB remitted to “where to seek care” thought- about as core issue of HSB. As an example, sample of items are given in the following “I visit health center when am really ill” and “I only visit health center for vaccination of my children”. “When I feel illness, I immediately visited health center”.

To measure HSB, likert scale was used with different degree of agreement. The degree of agreement are labeled as 1=strongly disagree, 2=disagree, 3=undecided, 4= agree and 5= strongly agree. Eleven items of questions were used to measure the health seeking behavior and perceived attitude of the respondents supported the role of CBHI system for health representation and health care needs, behavior towards health care service utilization. The higher mean score indicated that agree and strongly agree, the lower mean score indicated that disagree and strongly disagree in each provided items. Variable such a perceived health status was measured using the likert model agreement, the extent to which the degree of agreement marked 1 as low, 2 as medium, and 3 as good [44]. Finally, a list of FGD and KII guiding items were developed to bring out the lived experience of the participants about level of healthcare service utilization in range of CBHI schematic practice.

Qualitative Three focus Group Discussions (FGD) were conducted by taking insured and non-insured HH from the selected kebelle where quantitative data were not collected. Each group had eight groups of participants. The grouped were made up of three groups (two were from insured HH and the one group was from non-insure HH). The interview part was consisted of four participant (three of them are Tabya head managers, social workers and CBHI representative and the list one is head of Woreda health office), whose ages were ranged from 35 to 54 years. The data were collected by using audio recorder. Three data collectors were participated in the discussions. The first moderated all the sessions, the second person recorded verbal response of participants using audio recording instrument and the third person acted as note taker about socio demographic characteristics of participants and other necessary notes.

Variables Dependent variable was the outcome variable was the healthcare service utilization and enrolment status while the treatment variable was community based health insurance. While independent variables were:

- Socio-demographic factors of members of the participant such as age, educational status, family size, occupation, marital status, family member and outcome of the HH.

- Health care access related factor

- Health perception and health care needs variables (perceived health status and perceived quality of health care or health care seeking behavior)

- Income status Data Quality Assurance The questioner was administered by asking for the head of the household that have the most powerful in decision- making, his partner in the absences of the head of household. This view was managed and administered using local voice communication (Tigrigna) to facilitate the interview outgrowth. In the questionnaire, one scale was intensified to measure the perception of the respondents towards the CBHI system. The validity of the questionnaire was established using similar previous research based on the objective that has been done by Singh, 2017.

The questioner was tested on those who were 5% individual participant interviews before distribution of the data and therefore the trustiness was assured to possess uniformity. With respect to this, the soundness of the quantitative knowledge, the tools were engaged to stay the strength of the activity. Additionally, to the current, the pilot study was accustomed to augment the price of the question; the planning of the format, dimensions, and therefore the languages were accustomed to increase the responsibility of the information. The data collection was introduced to appropriate the constancy of the information. In other words, different strategies were accustomed to gather the qualitative data.

The data collectors were expected to construct a decent relationship, to explain the purpose of the study, to make a well-mannered relationship, and establishing smart environments with the respondents in respecting and polite ways to improve the believability of the information. Focus discussion and interview were utilized in order to possess a deep understanding. The questions were asked fastidiously by avoiding sensitive questions or problems.

The questioner was prepared in English version and translates into the Tigrigna language to determine the consistency. Consequently, the interpretation was assured through heedfully skilled people to skirt the difference in the sense of meaning, which means. The practitioners were approved, whether the study is repeated or not within a similar study area. Moreover, my classmates were taking a pledge by operating while not rest until the assignment end. The data collectors were assured the standard of the data by giving adequate coaching by the supervisor. Due to doing this, the type of CBHI and parts of healthcare service utilization of study members were set clearly. To cite my reference, Mendeley desktop info version 1.19.3 was used for making the great and acceptable catalogue.

Ethical Consideration Ethical clearance was obtained from Research Ethics Review Committee, school of social science and language, Mekelle University. Support letter has also obtained from both the Tigray regional and Woreda health bureau. Written consent was obtained from the study participants after explaining the research procedure to the study participants.

Method of Data Analysis

Quantitative and Qualitative Data Analysis

Mixed type of research approach was used to investigate the variables of interest.

Quantitative Data Analysis

First, once the data collection has administered, the quantitative data were cleaned, coded and e9ntered into SPSS for analyzing. The analysis was figured by using SPSS variant 21. Descriptive types of statistics were engaged to feature up the individual sampled. The analysis was carried out with descriptive statistics and inferential statistics. Every outcome of the variables was examined and at 95% of certainty was held off and the results were obtained from the analysis. The p-value; p<=0.05; it was assumed that a significant level of relationship and explains between the variety of socio-demographic features and the health care utilization of the respondents.

Descriptive Statistics

A descriptive form of statistic was used to describe the sample of health care service of characteristics of the community and varieties used by socio-demographic variables of the study participants; notably, percentages, graphs, and tables were used to describe demographic and health care service utilization among the respondents to describe the study population in relation to the appropriate variables. Herein once more, the measure of central tendencies were also introduced a bit like the mean, median and variance to observe the difference between the insured and non-insured households. Like age, sex, educational status, family size, occupation, legal status, and marital status and to get the difference in health care service utilization and this was established the individual intentions.

Inferential Statistics

Correspondingly, the inferential statistics like t-test (independent t-test), chi-square (χ2) and regression were disbursed to answer the remaining objectives. Here is that the independent t-test was accustomed to see whether the theme is reduced or not, or to assess whether the population mean is take issue by decreasing the impact of the confounders between the varied factors of health care service utilization among the insured and non-insured units. Therefore, this independent t-test was answered by addressing the objective one. The chi-square (categorical variables) was used to compute the association between the variations in utilization of health care service to compare variables that link between CBHI and health care service utilization among insured and non-insured households. Multiple linear regressions were used to analyze the effect of various health access variables relating to health care seeking behavior. In this section was assessed the leading items when to seek care and associating health seeking behavior of the insured and non-insured members were predominantly analyzed. In this vein, objectives of two and three were effectively addressed.

Qualitative Data Analysis/Thematic Data Analysis

Similarly, as the researcher observed that in the manner of quantitative records analysis, the qualitative data also have its very own way because raw data have no full of sense by itself unless it organized and analyzed properly. Therefore, to analysis qualitative data; the records were set for interviews and focal point crew dialogue in separate themes. Data were translated from Tigrigna to English language and then transcribed into narrative form. To analyzed the data; first prepare the data, splitting into manageable units, combine or synthesize it, probing or looking for patterns and locate out the extensive one. Hence, following the series of the data, write out the mobile-recorded information with the availability of note-taking activities. Understand and learn about all the transcript notes, major issues, necessary ideas and topics were identified and then the unprocessed statistics were categorized (bringing similar texts into meaningful units) based totally on the suitability of the thematic structure to which they recount. Then, in accordance with their similarity of the themes, the qualitative facts were integrated with quantitative information concomitantly primarily based on their goal plot.

Key- Informant Interview/KII

The KII was carried out with community-based health insurance managers/leaders and social workers found in the kebelle, in order to dig out with the number of factors of view. Members who have the next understanding of health care finance usually and CBHI theme carrying out specifically on key problems like apply and implementation, administration and the benefit of the package. The key informant interviews are participants who were provide information; what they comprehend or what it is going with the modern state of affairs of the issue, those who have first-hand data on their hand, involving the situation count number of the topic, presenting what the hassle looks like and was furnished recommendation in order to resolve the problems. The informant of qualitative research was select through using purposive sampling method until the saturated data is sufficient (Table 2).

| Name of the KII | Age | Sex | Position | Education | Work place | Date of interview | Length of interview |

|---|---|---|---|---|---|---|---|

| Asefa Belay | 40 | M | Leadership | Diploma | Atsbi | 4/5/2019 | 15 minute |

| G/Silasie Hishe | 36 | M | Social worker | Degree | Atsbi | 4/5/2019 | 0:10:12 |

| Tsegay Desta | 43 | M | Kebelle manager | 10th grade | Atsbi | 5/5/2019 | 5 minute |

| Kebede Beyene | 54 | M | Head of Woreda health office | Degree | Atsbi | 5/5/2019 | 18 minute |

Table 2: Socio-demographic of KI.

Focus-Group Discussion/FGD

In this study, focus group discussion was used in order to advocate higher information to perceive communities scene and dealing relating to advantage of the packaging, worth of services provision regards healthcare utilization and hospitalization of members by health care suppliers that the participant provides and acquire a wider field of soundness knowledge. Additionally in this type of discussion, they were raised about the payment and perception of the community towards the CBHI and issues were raised from side of non- members regarding knowledge towards the existence of CBH in their kebelle, access of information about the fairness of the prepayment and benefit towards the CBHI.

However, individuals view their knowledge, thoughts or any occurrences that happened in their lifestyle activities.

Whereas participant tend to use the FGD meeting because of its very valuable in providing the necessary information concerning what people feel/think or mirror what they are doing. A verbalized are going to be ready to lengthen info on the topic matter of the study regarding the gaps in the way to use the CBHI theme like, however they interact to become a member of the theme, the way to complete the insurance system , what’s the advantage are going to be gained from the theme. Additionally, to the present, quality health care service and their sight towards the CBHI schemes were investigated. Within the give-and-take, eight participants were collaborated with the optimum of about 30 to a pair of hours long. Throughout the study, participants had the liberty to talk to their own member (Table 3).

| Number of FGD | Sex | CBHI membership | Kebelle | Date of discussion | Place of discussion | ||

|---|---|---|---|---|---|---|---|

| Male | Female | Insured | Non-insured | ||||

| FGD one | 4 | 4 | 8 | - | M/Emba | 8/5/2019 | Kebelle administration office |

| FGD two | 2 | 6 | 8 | - | Kelisha | 8/5/2019 | Kebelle administration office |

| FGD three | 2 | 6 | 4 | 4 | A/Mesanu | 9/5/2019 | Kebelle administration office |

Table 3: Demographic characteristics of FGD.

Source: own survey 2019. Table 3: Demographic characteristics of FGD.

Results and Discussion

Data Presentation and Analysis

This section of paper introduced and analyzed the data gathered in order to search for a suitable answer for the objectives stated in the above chapter one. Hence, the current result used extraordinary sorts of tools to inspect the gathered data like the questioners, interview and FGDs. In the quantitative part, socio-demographic variables are calculated through using central tendency and dispersion each variable with aggregate of health care service and insurance status to assess whether each population character (age, sex, level of education, marital status, occupation and family size) have their own difference in the utilization of health care service among insured and non-insured HH. The Qualitative part includes both KII and FGD method. In the FGD part, the two-group members are consisted of eight individuals from insured HH whilst the third one is for non- insured HH, which entitled eight participants. This finding is approached using tables, frequencies, percentages and statistical descriptive such as mean and standard deviations for every item of query that accompanied with the aid of narrative explanation. In this study 172 HH member were participated with 100% response rate. Of the total, 50% of the participant were insured HH.

Back Ground Demographic Characteristics of Respondents

The back ground characteristics of respondents comprising of their age group composition, sex, educational status, marital status, occupation, family household size and income of household.

The age spectrum of participants in this study was 3.8, SD 0.788, and the majority 58.7% (N=101) of respondents were between 25-44 years old, 23.3% (N=40) were between 45-65 years old, the youngest 14.5 % (N=25) were between 18-24 years old. Besides, the remaining 46.6% (46) of group participants were within the age range of greater than 65 years old, among the insurance status majority (62.8%) were insured and (54.6%) were non-insured households.

Sex of the household participant was with mean of 1.76, SD 0.427 and the majority of them were female- headed respondents. The percentage of female respondents constitutes approximately 76.2% (131) of the total participant in the study, between both the insured (69.7%) and non-insured (82.5%). This means that of the total participants’ female-headed households were highly engaged in both the insurance scheme than male. This shows that females participants were more dominate in the utilization of healthcare service than male respondents because females headed HH is giving more emphasis on keeping the health of their families.

Concerning educational status, participants were within the average range of 1.24, SD 0.598 and among the total, 84.9% (N=146) of participants were unable to read and write, 6.4% (N=11) were allowed to read and write, 8.7% (N=15) were completed primary school and above. Among the majority of participants (82.5%) were included in the scheme and (87.2%) were non-insured. The more educated family has better knowledge towards the benefit of CBHI in using healthcare service more chance to gain awareness towards the benefit of healthcare service use by joining the nearest health institution rather than going to traditional medicines. This can maximize the personal health status of households. Apart from the matrimonial status of the participants, the average mean was 1.21 and SD 0.669, of which about 89% (N=153) were legitimately living with their families, 5.2% (N=9) were single, 1.7% (N=3), 4.1% (N=7) were widowed and divorced respectively due to different reasons but currently they were living with their children. The majority of the respondents were married, both among the insured married about (91.8%) and (86.0%) were insured and no insured respectively.

Concerning occupation, the average mean level of the respondent was 1.11 with SD of 0.452 and among them, majority 92.4% (N=159) respondents were assigned to agricultural operations, 5.8% (N=10) were traders and the remaining 1.7% (N=3) were unemployed. The majority of the respondents (farmers) (94.2%) were engaged in insurance while (90.1%) were not. The other determinant factor is the household respondent’s family size with an average mean was 1.65 and SD 0.477 and the highest 65.1% (N=112) were households family size with less than or equal to five (72.1%) insured and (58.1%) uninsured and 34.3% (N=59) were households with more than five family sizes.

As far as household income concerned, mean was 1.90 and SD 0.971 and only 5.2% (N=9) were incomes between 1001 and 3000, 52.5% (N=90) of income was less than or equal to 1000 birr; and the remaining 42.4% (N=73) of income was between 3001 and 5000. Among less or equal 1000 about (65.1%) insured and (39.5%) were not insured. People have greater capacity to outline and take advantage of extraordinary options if their profits are high. Assured people indicate that they are not optimistic about the future and want to shield themselves from the unusual incidence of health shocks at any time. If individuals have enough cash or earnings, they are not interested towards becoming a member of the insurance because they have the capacity and strength to any future health shock. People with good salaries or income will not be members of the CBHI scheme. As household revenue increases, the likelihood of involvement in the CBHI program declines.

In this analysis variable such as sex, family size and income of household showed a significant difference between the insured and non-insured households, however, factors like age, educational status and occupation did not show any deviation between insured vs. uninsured as shown in the (Table 4).

Socio-demographic characteristic Range Frequency Percentage Mean Standard deviation

18-24 25 14.5 Age

45-65 40 23.3 >65 46 46.6

Male 41 23.8

Sex

Total 172 100

Unable to read and write 146 84.9

Educational status

Primary education and above 15 8.7

Total 172 100

Married 153 89

Marital status

Widowed 3 1.7

Divorced 7 4.1

Farmer 159 92.4

Occupation

Jobless 3 1.7

Family status Greater than or equal 5 59 34.3 1.65 0.477 Less than 5 112 65.1

≤1000 90 52.5 Income of HH

3001-5000 73 42.4

- Source: Own survey 2019.

Table 4: Socio demographic characteristics of respondents.

Health is by nature the most delicate component. Everyone wants to save their lives from any pain that can damage them, and individuals are worried about it. Modern health organizations are suppliers of health care, which then attend to individuals for treatment from disease or injury. So that that people develop so that individuals create the habit of attending a health organization to examine their issue

3.18 0.778 25-44 101 58.7

1.76 0.427 Female 131 76.2

1.24 0.598 Able to read and write 11 6.4

1.21 0.669 Single 9 5.2

1.11 0.452 Merchant 10 5.8

1.9 0.971 1001-3000 9 5.2 and get health care to return to their prior health status. Therefore, in this analysis independent t-test was carried out between dependent variable and independent variables in order to compare the difference in health care service utilization between insured and non-insured households (Table 5).

| Variable | Range | Insurance status of households | Difference % | P value | |

|---|---|---|---|---|---|

| Insured % | Uninsured % | ||||

| Age | 18-24 | 12 (13.9) | 13 (15.1) | - | - |

| 25-44 | 54 (62.8) | 47 (54.6) | 0.055 | 0.628 | |

| 45-65 | 19 (22.1) | 21 (24.4) | -0.06 | 0.53 | |

| >65 | 1 (1.2) | 5 (5.8) | 0.005 | 0.99 |

Table 5: factor affecting both health healthcare service and enrolment among insured and uninsured households June 2019 (n=172

| Sex | Male | 26 (23.2) | 15 (17.4) | -0.176 | 0.049* |

|---|---|---|---|---|---|

| Female | 60 (69.7) | 71 (82.5) | 0.176 | 0.049* | |

| Educational status | Unable to read and write | 71 (82.5) | 75 (87.2) | 0.059 | 0.71 |

| Able to read and write | 6 (6.9) | 5 (5.8) | 0.055 | 0.79 | |

| Primary education and above | 9 (10.5) | 6 (6.9) | 0.41 | 0.41 | |

| Marital status | Married | 79 (91.8) | 74 (86.0) | -0.183 | 0.29 |

| Single | 3 (3.5) | 6 (6.9) | 0.183 | 0.29 | |

| Widowed | 1 (1.2) | 2 (2.6) | 0.183 | 0.533 | |

| Divorced | 3 (3.5) | 4 (4.6) | -0.88 | 0.65 | |

| Occupation | Farmer | 81 (94.2) | 78 (90.7) | -0.109 | 0.51 |

| Merchant | 4 (4.6) | 6 (6.9) | - | - | |

| Jobless | 1 (1.2) | 2 (2.6) | - | - | |

| Family status | Greater than or equal 5 | 23 (27.0) | 36 (41.9) | 0.164 | 0.042 |

| Less than 5 | 62 (72.1) | 50 (58.1) | -0.164 | 0.042 | |

| Income of HH | ≤1000 | 56 (65.1) | 34 (39.5) | -0.622 | 0.001* |

| 1001-3000 | 0 (0.0) | 9 (10.5) | 0.411 | 0.015 | |

| 3001-5000 | 30 (34.9) | 43 (50) | -0.211 | 0.007 |

Table 6: factor affecting both health healthcare service and enrolment among insured and uninsured households June 2019 (n=172

(T-test CBHI_ increase_ healthcare service utilization and enrolment), independent sample t-tests with no equal variances is assumed) Table 5: factor affecting both health healthcare service and enrolment among insured and uninsured households June 2019 (n=172).

Health Perception and Healthcare Needs

In terms of health and healthcare needs perception, the majority of 64 (74.0) insured and 69 (80.0) non-insured participants were considered as intermediate healthcare to provide accurate service from existing healthcare facilities, and few 12 (14.0) insured and four (5.0) participants received poor service from healthcare service providers because of affordability of drugs and other healthcare provision is very limited. Only 10 (12.0) insured and 13 (15) uninsured respondents were get good quality of service from current health facilities. Participants in the focus group discussions had knowledge toward the perception of healthcare service.

An insured father participant whose age is 47 years old said that: “Even though, our kebelle has good perception and better understanding towards the benefit of the package but in service delivery system is very poor due to some reasons. First, there is segregation between insured and non-insured ones because the healthcare service provider has favored to give good quality service for non-insured households. Why the reason is I do not know. Second, there is no access of drugs in our local area, and we always exposed to out-of-pocket expenditure by investing our money in non-public shops. In general, even I paid 700 to 800 ETB in private institutions; I completely recovered from my illness while in governmental health institution is not” (Insured FGD participant 2019). This idea supported and whose age 35 years old insured old mother said that:

Although CBHI (Community Health Insurance) has multiple benefits for our livelihood, some insured households have decided to stop their membership due to insufficient service provided by healthcare service providers. The absence of laboratory technicians and the replacement of experienced professionals with new ones have led to a lack of trust in CBHI among the community. This becomes problematic when diseases with similar symptoms, such as amoebiasis and giardiasis, and complicated acute febrile illnesses like typhus and typhoid fever arise, resulting in poor utilization of healthcare services among insured households (Insured FGD participant 2019).

With regard to perceived health status towards reliable service by kebelle representatives, a majority of 68 (79.0) insured and 70 (81.0) uninsured participants received intermediate service from kebelle leaders, while a few seven (8.0) insured and four (5.0) uninsured participants received poor service from kebelle leaders toward using CBHI.

Consequently, the majority 72 (84.0) insured and 48 (55.8) of uninsured participants noted that health institution takes as their primary preference to get better treatment. Of the total surveyed, two (2.3) insured and one (1.2) uninsured HH indicated that their primary option for curative intervention was traditional healers and very few one (1.2) uninsured HH also favored only water as their remedy. In addition, the remaining 12 (13.9) insured and 30 (34.9) non-insured respondent both going health institution and holly water takes as their treatment following about one (1.2) of non- insured respondents believes visiting health institution, traditional healers and holly water consider as their best treatment to get health service respectively.

In terms of current health status, the proportion of 70 (81.4) insured households were classified as healthy, while 44 (51.2) insured individuals were identified as normal, as individual insured household become more healthier because they have performed frequent medical checks on their health situation after they have been engaged in the CBHI system by decreasing pocket spending. In contrary, half 42 (48.8) percentage of the respondents were identified as not health, while few 16 (18.6) percentage of insured participant were recognized as not healthy, during this time respondents were got a service to follow up their condition of health at hospital and health center.

On the other side, factor in respondent exposure to chronic disease was subjected to chronic disease from 18 (20.9) participants, while eight (9.3) uninsured households were subjected to chronic disease such as diabetic disease, heart disease, and goiters. Similarly, majority 68 (79) insured and 78 (90.7) non-insured households were known with no chronic ill health and majority of them get service from the closest health institutions. Therefore, each respondent ought to say thanks for his or her god for not being exposed to chronic ill health. Concerning the expected health cost of recent treatment, few 12 (13.9) Insured and 26 (3.0.2) uninsured families were invested equal or more than five hundred birr. Especially the CBHI users subjected to an additional health cost, because healthcare providers were not provide equal and fair service between insured and non-insured households. Moreover, respondents also believed that, rather aiming to get service in governmental institutions they like to induce higher service in private clinics. In addition, respondents were not getting access of medication in their nearest health provided service but also insured households compelled to shop for medicine from non-public clinics and pharmacy. While the bulk of 74 (86.1) of insured and 60 (69.7) non-insured respondents were exposed below five hundred birr, during this case the insured households were gain a lot of profit as a result of already they are concerned in CBHI theme. This would be increase the healthcare service utilization by introducing the CBHI across the community. Regarding to the benefit of CBHI an interview carried out among Tabya head managers, political leaders and social workers, for example, a 36 years old male Tabya office manager explained that:

“The CBHI (Community-Based Health Insurance) scheme is crucial for the residents of the kebelle. This scheme provides affordable healthcare services to the community by allowing them to avail healthcare services from health centers and health posts. The residents can join this scheme by paying a small amount of 240 ETB per year, along with 10 ETB as registration fees. Despite the low cost, some people are still skeptical about the quality of service they would receive. However, the CBHI is critical for the community to access healthcare services”. (KII with kebelle head manager) In Line with the above argument, a 40-year-old male gave similar idea: “I believe that having a health insurance scheme is very important, especially if everyone is included, as it benefits those who are in non-insured households. As a diabetic patient, I used to face daily healthcare costs. However, since the introduction of the CBHI, I am fortunate to be part of the scheme, which helps me save money. After paying my dues, I received the required service as per my plate number 240 ETB. I’m grateful for this opportunity.” (Interview with vice kebelle Manager, 2019) Additionally, a 54 years old head of Woreda Atsbi- Womberta health office said that: “Our communities have greatly benefited from CBHI membership, not only because of the benefits but also because it is essential to establish good governance and create strong solidarity across the community. Due to financial insecurity, people in our Woreda lack access to drugs and some are forced to resort to finding access to holy water for treatment, which causes more suffering for the community. Meanwhile, some parts of the community receive healthcare services from the nearest private healthcare institution. Therefore, CBHI plays a crucial role in helping people. It serves as car payment insurance after any injury or harm has been received. Similarly, communities also pay 240 ETB before getting any illness or injury. For example, my brother Hagos Beyene slept in Ayder Referral Hospital for three months due to a complex severe disease. During this time, my brother had paid over 38,000 ETB by selling stocks like oxen and other animals from his home. Therefore, communities can save their money and start poor to get services equally with rich ones (KII with the director of Woreda Health Office 2019).” The study variables perceived health status towards reliable service provision, current level healthcare status, respondent exposed to current level healthcare status, chronic illness and expected healthcare cost of recent treatment were significantly vary among insured and un- insured households. However, variable like perceived quality of care, first choice of place for treatment during illness, perceived health status towards service provision by kebelle leaders were not significant variation comparing to household membership in CBHI (Table 6).

| Variables | Insured (%) | Uninsured (%) | Difference (%) | P value |

|---|---|---|---|---|

| Perceived health status towards reliable service provision | ||||

| Poor | 12 (14) | 4 (5) | -0.269 | 0.04* |

| Medium | 64 (74) | 69 (80) | -0.046 | 0.6 |

| Good | 10 (12) | 13 (15) | 0.046 | 0.053* |

| Perceived health status towards reliable service provision by kebelle leaders | ||||

| Poor | 7 (8) | 4 (5) | -0.144 | 0.363 |

| Medium | 68 (79) | 70 (81) | -0.014 | 0.8 |

| Good | 11 (13.9) | 12 (13.9) | 0.158 | 0.4 |

| Quality of care from get from health institution | ||||

| Poor | 7 (8) | 6 (6.9) | -0.032 | 0.8 |

| Medium | 76 (88) | 74 (86) | -0.173 | 0.3 |

| Good | 3 (3.5) | 6 (6.9) | 0.205 | 0.3 |

| Choice of place for treatment | ||||

| Health institution | 72 (84) | 48 (55.8) | 0.8 | |

| Traditional healers | 2 (2.3) | 1 (1.2) | ||

| Holly water | 0 (0.0) | 1 (1.2) | ||

| Health institution & holly water | 12 (13.9) | 32 (37.2) | ||

| Health institution, traditional healer &holly water | 0 (0.0) | 1 (1.2) | ||

| Current level healthcare status | ||||

| Healthy | 70 (81.4) | 44 (51.2) | -0.338 | 0.01* |

| Not healthy | 16 (18.6) | 42 (48.8) | -0.338 | 0.01 |

| Exposed to chronic illness | ||||

| Yes | 18 (20.9) | 8 (9.3) | -0.227 | 0.03* |

| No | 68 (79) | 78 (90.7) | 0.227 | 0.03 |

| Expected health cost of recent treatment | ||||

| Greater than or equal 500 birr | 12 (13.9) | 26 (30.2) | 0.236 | 0.01* |

| Less than 500 birr | 74 (86.1) | 60 (69.7) | -0.236 | 0.01* |

Table 7: Perceived needs to community based health insurance enrolment among respondent Atsbi-Womberta district, June 2019 (n=172

Source: own survey 2019. Table 6: Perceived needs to community based health insurance enrolment among respondent Atsbi-Womberta district, June 2019 (n=172).

Healthcare Access-Related Factors and Quality of Healthcare Provision towards Healthcare Service Utilization via Introduction Of CBHI

As the study showed that, majority 73.0% of insured and 53.0% uninsured participants were get service from health centers. However, participant get from hospital showed a significant difference between insured and uninsured household (for t=0.396, p=0.012). Particularly insured household were in favor of to get better service than visiting heath center and private clinic.

Regarding to access and Quality of health care service provision towards health care utilization, majority 57.0% insured household were get quality access of service when the distance is less five-kilometer from health facility and about 79.0% of non-insured households were get quality of access health care service when the distance is less or equal five- kilometer from health facility. To enroll in CBHI, households consider distance of health institution from home. As health, institution’s distance from home increases, individuals are opening up for extra transportation and other health-related expenses such as bedroom and food, then decreasing their interest.

Concerning a variable relating to time takes to closest health provision area from home in hours per adult person, half percentage 46.5% of the insured participant were time takes less than 30 minutes per adult person from home to closest health institution/health center to get heath access. In addition, 34.8% non-insured households were takes from 30 to 60 minutes per adult person from home to health center in order to get health access.

with regard to the affordability of payment towards CBHI, majority 84 (98.0) of insured respondents were believed that, the payment provided by the government is very affordable to insured households comparing to non- insured households because before the introduction of CBHI we were exposed to unnecessary health cost /out-of-pocket expenditure/ but now we are simply got service with simple cost. Similarly, 64 (74.4) of non-insured respondent reported that the payment offered with government of Ethiopia is very fair and affordable but we could not joined that why the reason is because we did not give much concern towards the benefit of the scheme or due to negligence. To support this idea, group discussion has made regarding the affordability of payment towards CBHI scheme. For instance, a 56-year-old male clarified his view as follows; among the group debate.

“CBHI offers great benefits to those who are involved in the scheme. Only a small fee of 240 ETB is paid annually, covering all the expenses for the year to treat my family’s illnesses. Before joining CBHI, we were subjected to unnecessary healthcare costs, but now we are fortunate to have saved money and minimized our stress. I live with eight families, and all of us are members of CBHI. However, only two of my mature children live separately from their own homes and only 50 ETB helped me to get such an important service.

For instance, my wife was suffering from severe pneumonia and was hospitalized in Mekelle for two weeks. During that time, CBHI covered the cost of 8,000 ETB, and my wife was able to receive the necessary treatment and fully recover from the disease. Therefore, the payment provided by CBHI is affordable and has helped me save a significant amount of money. This has been a great relief to me and my family. (Insured FGD participant 2019).

Furthermore, a 45-year-old second FGD respondent said, “I understand that you would like me to rewrite the text you provided to make it clearer. Here’s the corrected version:

“All in all, the Community-Based Health Insurance (CBHI) payment is very affordable just as my colleagues have described. However, I would like to add that the government’s efforts in enforcing the CBHI policy and strategy in our kebelle are highly appreciated. Before the introduction of CBHI, I had to pay exorbitant costs when seeking medical services from private dispensaries and medical centers. For instance, I had to pay 100 ETB for an ID card before receiving any service or medication. This was unreasonable for the impoverished society I live in. After the government introduced CBHI, I only have to pay 240 ETB once a year. Therefore, in our kebelle, CBHI has helped to reduce out-of-pocket expenses. However, there is a problem with healthcare service delivery by healthcare providers. They often prescribe drugs without proper diagnosis.” Also a third FGD participant said that “The payment provided by CBHI is very reasonable and affordable. For instance, I have four children at home. One of my children got injured in a motorbike accident in Atsbi town, near Street lion bank. I was immediately taken to the nearest healthcare facility and didn’t have to pay a single cent because of my membership. My child received free treatment. Therefore, I would advise everyone to join the scheme as soon as possible because I have experienced first-hand the benefits of CBHI.” However, very few 2 (2.3) insured participants have been stated that the quantity of payment given is very costly because not all individuals are able to get cash to pay for CBHI, and some insured participants have also said that this payment is not fair to some individuals because some part of the communities are not secure about food. Even some folks have no source of income throughout the year. Therefore, instead of covering the CBHI they just prefer to purchase a regular food. That is why the state should bring the CBHI to be a member free of charge as well as the deposit paid every year. Additionally, about 22 (25.6) of the non-insured participant noted that, because the payment provided is not affordable and unbelievable in service delivery, so that we are not allowed to be part of the scheme.

During a focus group discussion, a fourth participant mentioned that “It is important not only to save costs but also to seek medical attention at health centers as soon as possible when feeling unwell. They expressed their satisfaction with the service they received at 240 ETB and appreciated being able to receive medical care with their loved ones. However, they pointed out that there is a problem with medical professionals being reluctant to refer them to other medical institutions such as hospitals. As a result, they were forced to discontinue their CBHI membership due to these challenges”. This statement was made by a non-insured participant during the FGD in 2019.

In terms of receiving better healthcare services, a majority of 76 (88.4) insured families were thought to be receive better healthcare services from those who are insured respondents than non-insured families because being engaged in CBHI they merely minimized the out-of-pocket expenses. To support this suggestion just explained by FGD participants, among FGD participant: a 59 years old female participant was forward an idea regarding better service health care service between insured and noon-insured households via health care providers “Our government has implemented a good structural policy and strategy of CBHI which has benefited us at low and fair cost. I am very grateful for this and we hope to have its full sustainability. Since becoming a member of CBHI, I have not had to pay for any health care services. However, some healthcare providers are slow in providing healthcare services and some tend to give better service to those who are not insured. In some cases, healthcare providers could not give us the prescribed drugs and asked us to buy them from private pharmacies instead, while non-insured persons simply got access to them in the same institutions.” (Insured female FGD participant 2019).

In the opposite side with the above discussion, one FGD respondent whose age was 64 years old said that “Insured households tend to have more savings as compared to non-insured ones, as they pay a certain amount every year to remain insured. In my experience, healthcare providers have treated me well and I have no complaints about the services they provide. I only request that they treat me equally to those who are not insured. This quote is from a male participant in a focus group discussion held in 2019.

While 16 (18.6) of insured households believed that insured households do not receive better healthcare services than uninsured households do because healthcare providers tend to provide better service to uninsured households. Since heath providers consider that the non-insured has the potential to pay regularly, so that the non-insured households have given priority to receive better service than those of the non-insured. Similarly, in addition to the view of non-insured homes, majority 70 (81.4) of non-insured homes have been suggested that insured families receive better healthcare services than non-insured homes because the payment paid for CBHI is very simple and there would be no extra payment if they once paid the payment once a year.

As a result, factor like distance taken from health facility (for t=-0.385, p=0.001), service get from nearest health institution which is hospital (t=0.396, p=0.012), affordability of payment (t=, p=0.001), getting of better service (t=, p=0.001) and travel time from home to health institution varies significantly with households CBHI enrolment (Table 7).

| Variables | Range | Insured (%) | Uninsured (%) | Difference (%) | P value |

|---|---|---|---|---|---|

| Nearest health institution (service get) | Health centre | 46 (53) | 63 (73.0) | 0.578 | 0.249 |

| Private clinic | 1 (1.2) | 0 (0) | -0.182 | 0.676 | |

| Hospital | 9 (10) | 2 (2.3) | 0.396 | 0.012 | |

| Distance from health facility | <5 KM | 49 (57.0) | 18 (21.0) | -0.385 | 0.001* |

| ≤5 KM | 36 (42) | 68 (79) | -0.385 | 0.001* | |

| Travel time in hours | <30 minutes | 40 (46.5) | 30 (34.8) | 0.076 | 0.466* |

| 30-60 minutes | 22 (0.25) | 12 (13.9) | -0.076 | 0.0462* | |

| 1-3 hours | 21 (21) | 31 (36) | -0.168 | 0.068 | |

| 3-6 hours | 3 (3.5) | 13 (15) | -0.384 | 0.075 | |

| Payment of CBHI | Yes | 84 (98.0) | 64 (74.4) | -0.698 | 0.001* |

| No | 2 (2.3) | 22 (25.6) | 0.698 | 0.001* | |

| Getting of better service due CBHI | Yes | 76 | 10 | -0.698 | 0.001* |

| No | 16 | 70 | 0.698 | 0.001* |

Table 8: Healthcare access-related factors and Quality of healthcare provision and enrolment.

Reason/S for Membership/Not to Community Based Health Insurance

Insured Members were questioned why they joined the CBHI system to find out why they were members. Multiple decisions were made to define different reasons for becoming a member of the CBHI system. Multiple responses were offered, 75 (87.2) participants joined the system owing to extremely exposed families to healthcare costs, five (4.7) participants were subjected to injury-related disease and few five (5.8) participants were due to disease and those are extremely exposed to healthcare costs, Similarly, 2.3% and 4.7% owing to disease and low and fair payment. To support the idea, FGD explained why they preferred to become a member of CBHI. For example, a 60-year-old woman was given the reason:

“I am a member of CBHI due to a disease or injury that commonly occurs in our home. Additionally, we are not financially secure at the moment. Therefore, I felt the need to be a part of the scheme as I only have to make a one- time payment and not worry about any extra payments throughout the year.” Regarding to non-insured household, Participants were discussed why they joined the CBHI system to find out why they were not members. There have been several options to delineate different reasons for not becoming a member of the CBHI system and the prime reasons were first, The proportions of non-insured participants 56 (65.1) did not join the system due to absence of awareness and about 13 (15.1) of participants did not join due to no pressure from the CBHI office (Table 8).

| Reasons for membership | Frequency | Percentage (%) | Mean | Standard deviation |

|---|---|---|---|---|

| Illness due to injury | 4 | 4.7 | 2.21 | 0.984 |

| Exposed to healthcare cost | 75 | 87.2 | ||

| Premium is low | 2 | 2.3 | ||

| Due to illness and exposed healthcare cost | 5 | 5.8 | ||

| Reason for non-membership | 5.45 | 1.508 | ||

| Do not expose to any illness | 4 | 4.7 | ||

| we have enough money for treatment | 3 | 3.5 | ||

| No pressure from family member | 13 | 15.1 | ||

| No pressure from CBHI office | 1 | 1.2 | ||

| No awareness | 56 | 65.1 | ||

| Do not expose to any illness and we have enough money | 6 | 7 | ||

| Negligence | 3 | 3.5 |

Table 9: Reason/s for membership/not to community based health insurance.

Health Seeking Behavior among Insured and Non-Insured HH Toward Healthcare Service Utilization

The level of health seeking behaviours was assessed among the insured and non-insured households toward using healthcare service utilization. HSB has more emphasis in increasing the health care utilization because healthcare service utilization is the ending point of health seeking behaviour. Eleven items were assigned to “when seeking care” as the key factor of HSB. Independent sample t-tests with equal variance were calculated to see the difference if the implementation of the plan is increasing the health care service utilization by assessing the health-seeking behaviour of the insured families. Each item question of HSB with high mean score indicated that agree and strongly agree and respondents with lower mean showed that disagree and strongly disagree [45].

With regard to this analysis, there was significant result on HSB between the insured and non-insured households (t=0.023, p=0.05). In particular, only one somewhat variable categorized by the insured participants shows significance difference and where in favor of “when I feel sick I immediately visit health centers” as compared to non- insured households. However, the remaining ten items of seeking care rarely shown low response from taking care of an immediate action during illness their illness.

Result shown from the table, almost all measure of perceived health seeking behavior except Q5 did not show significant difference comparing to insured and non-insured households. For instance, household visited for health institution for simple illness like flu and early consultation, visit health center when am really, for vaccination of my children and including q4, q6, q7, q8, q9, q10, and q11 did not have any significant differences to health seeking behavior (Table 9).

| Measure of perceived health seeking behaviour ( when to seek care) | Insurance status | Independent t-test | |||||

|---|---|---|---|---|---|---|---|

| Insured | Non insured | ||||||

| Mean | SD | Mean | SD | Df | Sig | P</t</** | |

| Q1. I visit health centre when am really ill | 3.99 | 1.023 | 4.19 | 0.604 | 170 | 0.05 | 0.125 |

| Q2. Only visit health centre for vaccination of my children | 2.33 | 0.818 | 2.43 | 0.902 | 170 | 0.05 | 0.426 |

| Q3. For simple illness like flu I visit health centres | 3.7 | 1.096 | 3.38 | 1.432 | 170 | 0.05 | 0.125 |

| Q4. For any illness, I make an early consultation to avoid further risks | 3.77 | 1.195 | 3.4 | 1.417 | 170 | 0.05 | 0.064 |

| Q5. When I feel sick I immediately visit health centres | 3.78 | 1.287 | 3.31 | 1.374 | 170 | 0.05 | 0.023 |

| Q6. During my illness, I rarely Seek help from professionals | 3.59 | 1.458 | 3.22 | 1.458 | 170 | 0.05 | 0.096 |

| Q7. No matter the type of illness, I used to see health centre after days | 3.2 | 1.548 | 3.21 | 1.535 | 170 | 0.05 | 0.961 |

| Q8. When I feel, ill I am almost certain to visit health centre | 3.67 | 1.451 | 3.77 | 1.28 | 170 | 0.05 | 0.671 |

| Q9. When I have any health problem, initially I either do not do anything or try some home remedy | 3.48 | 1.501 | 3.63 | 1.439 | 170 | 0.05 | 0.501 |

| Q10. My family has good value for usual check up | 3.7 | 1.431 | 3.91 | 1.252 | 170 | 0.05 | 0.309 |

| Q11. I do whatever is necessary to be as healthy as I possibly can be | 3.78 | 1.397 | 3.84 | 1.299 | 170 | 0.05 | 0.802 |

Table 10: Measure of perceived health seeking behaviour “when to seek care” among insured and non-insured respondents in Atsbi-Wom

Healthcare Service Utilization among Insured and Non-Insured Households

This analysis showed that, due to the introduction of effective CBHI, the majority of 86 (100.0) of insured household participants used the healthcare service, and 67 (77.9) uninsured respondents used the health care service, but only 19 (22.1) uninsured households did not use health care. This means that in the past six months before to data collection, household were enrolled in CBHI (56.2%) were more probable to use health care service than households who were not enrolled (43.8%) (χ2=21.359, p<0.001) as shown in Table 10. While the result shows, the level of health service utilization of CBHI among insured members is better than the non-members are for not only the untreated members but also even based on number of treated individuals attributable to their illness in both groups.

| Variable | Range | Health service utilization | |||

|---|---|---|---|---|---|

| Yes (%) | No (%) | χ2 | P value | ||

| Insurance status | Insured (%) | 86 (100.0) | 0 (0.0) | 21.359 | <0.001* |

| Healthcare service utilization (%) | 56.20% | 0 | |||

| Uninsured | 67 (77.9) | 19 (22.1) | |||

| Healthcare service utilization (%) | 43.80% |

Table 11: Healthcare utilization and community health insurance enrolment in Atsbi Womberta district, June 2019 (n=172).

Discussion

The purpose of this research was to compare the use of healthcare services among CBHI members of insured homes and non-insured homes and identify associated factors for CBHI enrolment in Atsbi-Womberta District. A mixed research approach used to collect data from 172 respondents (86 insured HH and 86 non-insured HH) using questioners, KIIs and FGDs. As a result, primary data from the above- mentioned participants and informants gathered to tackle the research objectives.

As per data obtained from either the social and economic-demographic survey, the majority of participants were women, as decision-making power becomes more common in rural areas for male and public activities more decided by males as per the female respondent’s information. Nevertheless, some male respondents were not found during the time of data collection. As far as age was mentioned, the majorities (62.8%) of participants were between 25 and 44 years of age, and most of the respondents (91.8%) are married. Regarding the size of the family, respondents (72.1%) have a family size of less than or equal to five insured members and most respondents (87.2%) are unable to read and write; this is common in most rural societies.

In this ponder; the families selected in CBHI were more likely to utilize health services than the families not enlisted in CBHI. The rate of healthcare service utilization was higher among families who were individuals of a risk-sharing institution. This result was consistent with the study finding conducted in North-West Ethiopia.

In this study, a higher number of study subjects with chronic illnesses were observed among the insured households than the uninsured household. This finding was similar with a study done in Ghana [46] in the insured households; the status of chronic illness was higher than that of uninsured households.